You're likely taking familiar steps when a move gets real. You've opened a dozen tabs, every company says it's professional, every quote sounds reasonable at first, and every website uses the same words: careful, reliable, affordable, licensed, insured. The problem isn't finding movers. The problem is figuring out which one will show up with the right truck, the right crew, the right paperwork, and the right accountability if something goes wrong.

That's where people get tripped up. They assume “licensed and insured” is just a marketing phrase, or they stop after spotting a DOT number on a website. In practice, that phrase only matters if you verify it and understand what it does, and does not, protect. A mover can sound polished on the phone and still leave you exposed to hidden fees, subcontracted labor, weak liability coverage, or a claim process that disappoints you after the damage is done.

I've seen customers focus hard on price and timing, then ask about credentials as an afterthought. That's backwards. Before you compare estimates, before you read promises on a homepage, you need to know how to separate a real operator from a risky one. Reading verified Boston mover reviews helps, but reviews should support verification, not replace it.

The High Stakes of Choosing Your Mover

A bad move rarely starts with obvious chaos. It starts with a low quote, a rushed phone call, and a promise that “everything is covered.” Then moving day arrives and the truck is unmarked, the crew doesn't match the company you thought you hired, and the final bill starts changing after your furniture is already loaded.

That's why the phrase licensed and insured movers matters so much. It isn't industry jargon. It's the dividing line between a company that can be held accountable and one that can disappear behind excuses, subcontractors, and vague paperwork.

Most customers don't need a lecture on regulations. They need a reliable answer to one question: Can I trust this company with my home, my belongings, and my timeline? Trust in moving is never built by slogans alone. It's built by records you can verify, insurance you can confirm, and documents that explain responsibility before the first box leaves your home.

Practical rule: If a mover gets irritated when you ask for license and insurance details, stop there. A legitimate company deals with those requests every day.

The risk gets higher when you're stressed, in a hurry, or moving during a busy season. That's when people accept vague estimates, skip reading the bill of lading, or assume “insured” means full replacement if a valuable item is damaged. It doesn't. That misunderstanding alone causes a lot of expensive disappointment.

A professional mover should make verification easy. You shouldn't have to chase basic documents, decode evasive answers, or guess who's responsible for what. If you do, you're already seeing the kind of operational disorder that causes trouble on moving day.

What Licensed and Insured Really Means

On paper, almost any company can say it is licensed and insured. The actual question is whether those words hold up when a truck is late, a dresser is damaged, or someone gets hurt carrying a sofa down a Boston triple-decker stairwell.

Licensed means the company has legal authority for the type of move it is selling

Licensing is specific. A mover handling interstate jobs needs federal operating authority and a U.S. DOT number. A company doing local household moves in Massachusetts has to meet state requirements, not just print a logo on an estimate. Those are not interchangeable.

Scam operations often borrow the appearance of legitimacy. They list a DOT number that belongs to another carrier, operate under a different business name than the one on the truck, or act as a broker without saying so. A legitimate mover should be able to tell you the exact name its license is filed under, whether it is the actual carrier, and whether your move stays within Massachusetts or crosses state lines.

If those answers are vague, treat that as a warning sign.

Insured means there is real financial backing, but you still need to ask what is covered

Insurance protects against certain losses tied to the mover's operations. It does not automatically mean your belongings are covered for full replacement cost. That is where many customers get burned.

A professional company should be able to explain, in plain English, whether it carries general liability insurance, workers' compensation where required, and cargo-related protection or valuation options for the shipment itself. Those are separate issues. If a salesperson uses “fully insured” as a blanket answer and cannot explain the difference, the problem is not just poor communication. It usually points to weak office training or a company that expects the customer not to press for details.

I tell customers to listen for specificity. Real operators answer with policy types, coverage purpose, and written documents. Risky operators answer with slogans.

The same standard applies in other trades that work inside occupied homes. Verified credentials matter because they show that the company can be checked, not just trusted on its word. That is the value behind official IICRC certification details, and the logic carries over to moving.

The practical difference is accountability

A licensed mover can be traced through its registration, operating name, and complaint history. An insured mover has policies that can be requested and verified by a landlord, condo association, or customer. That paper trail provides you with recourse if something goes wrong.

Without it, you are often dealing with a phone number, a deposit request, and a crew that may disappear after delivery. That is why “licensed and insured” should never be treated as a marketing phrase. It is a baseline test of whether the business can be held responsible for your home, your shipment, and the people it sends onto your property.

The Three Types of Mover Protection You Must Know

It's common to hear “insured” and assume one broad shield covers everything. That's not how moving works. There are several layers of protection, and each one handles a different problem.

General liability protects the property around the move

General liability coverage usually addresses accidental damage caused during the work that affects third-party property or the premises. If a crew gouges a building wall, cracks a lobby tile, or damages part of a common area while carrying furniture, this is the category you want to know about.

For apartment and condo moves, this matters a lot. Building managers often ask for proof of insurance before allowing a move because they know hallways, elevators, entry doors, and loading areas are vulnerable on moving day. When a mover can't provide a clean certificate of insurance, that creates friction immediately.

Cargo insurance and valuation are different things

Customers often misunderstand this distinction. Insurance and valuation are not the same thing. Federal guidance explains that basic value protection may cap liability at $0.60 per pound per item, so a damaged 100-pound piece of furniture could be covered for only $60 under that default structure. Full Value Protection provides greater protection, but you must select it and pay for it. The FMCSA lays that out in its valuation and insurance guidance for household moves.

North Carolina's mover guide also explains the distinction well on the state side. It says intrastate movers must carry at least $50,000 in cargo insurance, while basic value protection may still cap liability at $0.60 per pound per item, and full-value protection can require replacement, repair, or market-value compensation depending on the situation. That's why consumers should verify cargo, liability, and workers' compensation coverage, then read the shipment terms before signing, as described in the state's mover guide on insurance and valuation.

Here's the cleanest way to look at the two common liability options:

| Feature | Released Value Protection | Full Value Protection |

|---|---|---|

| Cost | Included at no additional charge in the standard liability framework | Costs extra |

| Liability basis | Minimal protection based on weight | More comprehensive protection |

| Example outcome | A 100-pound item may be covered for only $60 | The mover's obligation can be replacement, repair, or market-value compensation depending on terms |

| Best for | Customers who knowingly accept minimal recovery | Customers who want stronger financial protection for their shipment |

A useful mental model comes from other custody-based businesses. If you've ever looked at essential bailee coverage for auto dealerships, you've seen the same principle. The business may have insurance for its operations, but the customer still needs to understand what protects the property left in that business's care, custody, and control.

Don't ask only, “Are you insured?” Ask, “What covers the truck, what covers my shipment, what covers building damage, and what valuation option am I signing?”

Workers compensation protects you from a different kind of problem

Workers' compensation often gets ignored by customers because it sounds like an internal company matter. It isn't. If a mover gets hurt carrying your furniture, you want the employer's workers' compensation system in place rather than loose ends and liability disputes.

This isn't a theoretical concern. Industry guidance notes that licensed carriers are generally expected to carry auto, cargo, and general liability insurance, and many also carry workers' compensation coverage. The same discussion cites the Bureau of Labor Statistics report of 184,470 injuries among transportation and material-moving workers in 2018, which is one reason consumers are told to verify insurance rather than assume every moving company offers the same protection, as summarized in this licensed and insured mover guidance.

Why Hiring Licensed Movers Is Non-Negotiable

At 6 p.m. on moving day, the truck is loaded, your lease is ending, and the foreman says the price just changed. If the company is properly licensed, you have a business identity you can trace, rules that apply to the move, and a paper trail that matters. If it is not, you are arguing with a phone number and a logo.

That is the practical reason licensing matters. It gives the customer something to verify before the job and something to point to if the job goes sideways.

Moving attracts a lot of small operators, and many do honest work. Some do not. In a crowded field, a clean website, a low estimate, and a friendly salesperson prove very little. The test is whether the company is legally authorized for the work it is selling and whether that authority matches the move. Interstate household goods moves require federal authority. Local household goods moves in Massachusetts raise a different set of state-level questions, which many generic articles skip.

A proper license also changes your position in a dispute. It ties the mover to a legal business name, a recorded operating history, and specific obligations tied to the type of job. That matters when there is a missed delivery window, a surprise charge, damaged property, or a shipment that is being held until you pay more than the estimate led you to expect.

I have seen customers focus on blankets, dollies, and truck size, then skip the credential check. That is backwards. Equipment affects efficiency. Licensing affects whether you hired a legitimate carrier or a risky operator pretending to be one.

The other point customers miss is fit. “Licensed” by itself is too vague to be useful. The authority has to fit the job being sold. If a company is quoting an interstate move, local authority alone is not enough. If the company is taking your goods into storage, ask who holds custody during that period and under whose authority that part of the job is being performed. If subcontractors are involved, get the legal names before you sign anything.

Unlicensed movers create ugly problems fast. They can disappear after taking a deposit. They can show up under a different company name than the one on the estimate. They can load first and renegotiate later, when your furniture is already on the truck and your options are gone. By the time a customer learns the operator was not properly authorized, the pressure is already at its highest.

Licensing does not guarantee good service. It does give you a way to screen out many bad bets before they get inside your home. That alone protects a lot of people from avoidable loss.

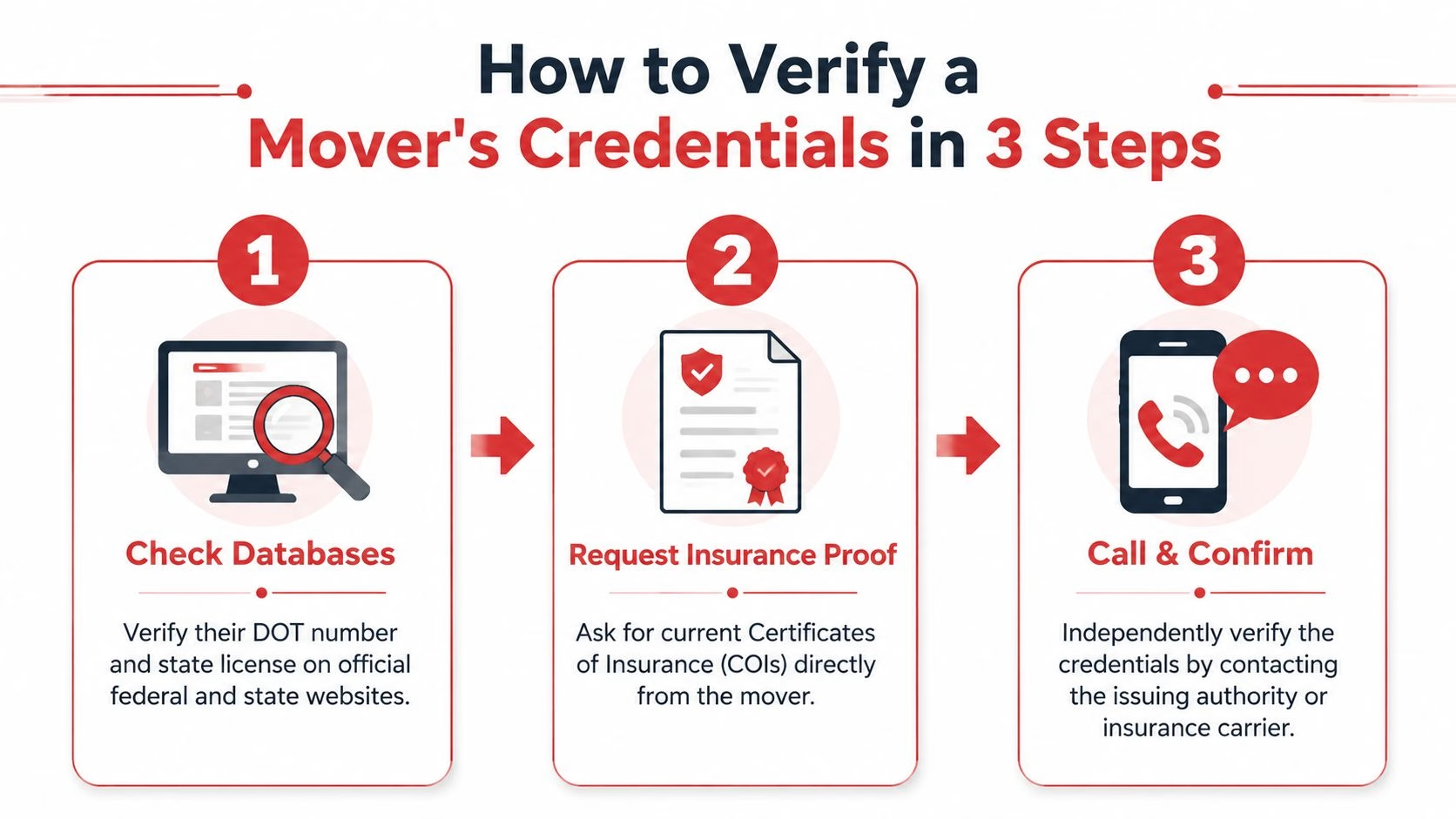

How to Verify a Mover's Credentials in 3 Steps

Verification doesn't need to be complicated. It needs to be deliberate. If you follow a short process and insist on documents instead of promises, you'll eliminate most bad options quickly.

Step 1 check the right database for the type of move

For an interstate move, start with the federal database. Ask for the company's legal business name and U.S. DOT number, then verify it in the FMCSA system. Don't rely on a logo, a screenshot, or a number pasted into a quote. Match the number to the business name and confirm the authority aligns with the service you're buying.

For a local Massachusetts move, you also need to confirm state-level authority for intrastate household goods moving. In Massachusetts, that means checking the mover's standing with the Department of Public Utilities, Transportation Oversight Division, and confirming the business has the proper MA DPU operating authority for local household goods work.

If you want a good non-moving example of why license checks matter, HomeProBadge's contractor trust guide explains the same consumer principle clearly. A license only protects you if you independently verify it with the authority that issued it.

Step 2 ask for the insurance certificate not just verbal assurance

A legitimate mover should provide a current certificate of insurance, often called a COI. If you're moving into a condo building, managed apartment, or office property, the management company may ask for one anyway. That requirement helps you because it forces the mover to document coverage in writing.

When you review a COI, look for a few basics:

- Business identity: The named insured should match the mover's legal business name, not an unrelated company.

- Policy status: The coverage should be current on the date of your move.

- Coverage types: Look for general liability and auto coverage at minimum, and ask directly whether cargo and workers' compensation are in place.

- Certificate holder details: If your building needs to be listed, confirm the mover can issue an updated certificate correctly.

A company that says “don't worry, we're fully covered” but hesitates to send a COI is giving you information you can't use. Paperwork is what counts.

For example, some customers reviewing Boston-area options ask for operating credentials and third-party trust signals together. One public-facing reference point is this BBB certificate page for TLC Moving & Storage in Massachusetts, but the broader lesson is the same for any company you consider: verify documented credentials, don't just absorb reassurance.

Step 3 confirm who is actually performing the move

This step catches a lot of scams. Ask one direct question: Are you the carrier moving my goods, or are you a broker arranging the move? Then ask whether your shipment will stay on one truck, whether labor is subcontracted, and whether storage or transfer points are involved.

Consumer complaints often start with confusion at this exact point. The company that sold the move wasn't the company that showed up. Or the shipment changed hands and the customer lost visibility, control, and recourse. If the mover answers vaguely, that's your cue to walk away.

Call the office and ask the same operational question two different ways. Solid companies answer consistently. Sloppy or deceptive ones don't.

One practical way to test professionalism is to ask for the names of the documents you'll receive before move day. A real mover should mention the estimate, order for service if applicable, and bill of lading, then explain who issues them and when.

Your Hiring Checklist and Common Red Flags

The bad hires usually reveal themselves before move day. A rushed estimate, a fuzzy company identity, or a crew that does not match the paperwork is how customers end up arguing over charges with their furniture already on the truck.

Green lights before you book

Use this checklist before you pay a deposit.

- Written estimate: Get the quote in writing. Make sure the inventory, addresses, dates, and services match what you requested.

- Clear legal identity: Confirm the exact legal business name, not just the website name or the name printed in an ad.

- Confirmed carrier: Verify who is physically handling the shipment. If one company sells the job and another company shows up, risk goes up fast.

- Insurance paperwork: Request the COI early if your condo, apartment, or management company requires one. A legitimate mover should know how to produce it without confusion.

- Bill of lading review: Read the liability and valuation language before move day, not while a crew is waiting in your driveway.

- Site-specific details: Ask about stairs, long carries, elevator reservations, storage, shuttle trucks, packing, and specialty pieces such as safes, pianos, or glass tops.

- Boston-area planning: For city moves, ask how the company handles parking permits, narrow streets, building time windows, and certificate requirements.

TLC Moving & Storage is one example of a Boston mover that presents itself as handling local moves, interstate work, packing, storage, and specialty items. Treat that as a scope check, not a sales claim. Compare the same details across every company you vet so you know who is equipped for your job.

Red flags that should stop the conversation

Some warning signs are serious enough to end the call.

- Vague answers about broker versus carrier: If the office cannot clearly explain whether it is the actual mover or just arranging the job, walk away. That confusion sits behind a lot of moving disputes, including the problems described in this warning on brokers and unlicensed movers.

- No real business footprint: A mover should have a verifiable address, working office phones, and a business presence that lines up across its documents.

- Unmarked truck or mismatched crew: If the truck has no company identification, or the crew name does not match the company you hired, stop and call the office before anything is loaded.

- Pressure around paperwork: No professional mover should discourage you from reading documents, checking totals, or confirming valuation coverage.

- Foggy claims process: If the company cannot explain who handles claims, what deadlines apply, and what documents you would need after damage or loss, expect problems later.

- Large deposit demands in odd forms: Be careful with operators who push for large cash deposits, payment apps, or immediate payment before they have done any real work.

A clean estimate means very little if accountability disappears the moment something goes wrong. The right mover makes verification easy. The wrong one makes every basic question feel like a hassle.

Moving in Boston and Massachusetts A Local Guide

National advice only gets you halfway there. In Massachusetts, a local household goods move calls for a closer look at state authority, and in Boston, local logistics can turn an ordinary move into a difficult one fast.

What to check for local Massachusetts moves

For an in-state household move, ask for the mover's Massachusetts DPU authority and verify it through the Department of Public Utilities, Transportation Oversight Division. Don't treat an interstate DOT number as a substitute for local compliance. The move has to be authorized for the actual lane and service you're buying.

If you're comparing local options, ask one more question that generic guides often miss: Will the same company that books the move be the same company and crew handling the move? That matters even more when storage, multiple stops, or specialty pieces are involved.

Boston logistics punish inexperienced movers

Boston is not forgiving to sloppy operations. North End streets, Beacon Hill access, narrow driveways, older triple-deckers, reserved loading windows, freight elevator rules, and condo COI requirements all demand planning before moving day. A crew can be honest and hardworking and still cause delays if the company didn't prepare for the city.

Customers moving within Greater Boston should ask whether the mover helps coordinate street occupancy permits, building certificates, elevator reservations, and truck access strategy. Those details don't sound dramatic until a truck can't park legally near the address or a building denies access because the COI is wrong.

If you're planning a neighborhood or suburb-to-city relocation, a Massachusetts-focused planning resource like this guide to local moving in Massachusetts can help you think through timing, access, and building logistics before the move is booked.

If you want a mover that treats credentials, insurance, paperwork, and logistics like the core of the job, not an afterthought, talk to TLC Moving & Storage. Ask direct questions, request the documents, and make sure the company you hire can prove exactly how it protects your home, your shipment, and your schedule.

Recent Comments